Index Funds as Productive Assets

Some thoughts on how index funds can be productive for the holders

Previously published in my old Blog - 05th November 2020

Introduction

Productive assets are ones that generate profits and cash flow. Farmland, rental properties, and dividend-paying company shares are all productive assets. Non-productive assets don’t produce income but may have other properties that are valuable. Gold is the classic non -productive asset that manages to retain its value.

However, nonproductive assets can be used to generate income. Gold can be used as collateral to raise a loan to invest elsewhere. So, I like to consider the intrinsic and extrinsic properties of an asset.

Intrinsic and extrinsic productivity in crypto assets.

Few crypto assets have high intrinsic productivity. Some, like $MKR, have a buyback and burn economic model that rewards the passive holder by reducing the overall supply and maintaining an ongoing buying pressure.

Many more tokens have an income generation mechanism built within tokens economics. This could include rewarding staking in a no-risk governance contract ($YFI), staking with the potential for slashing ($AAVE) or rewarding ongoing activity ($SNX, $KNC). However, some of these mechanisms include timelocks on the deposited tokens.

Then there are external mechanisms that allow income to be generated. E.g. many tokens can be deposited as collateral within AAVE or Compound to generate income, or into a MakerDAO vault to allow DAI to be minted. While these opportunities are totally independent of the token, their existence and the composability of DeFi means that the fund tokens have the ability to be extrinsically productive.

Bitcoin is generally considered a passive store of value akin to gold. i.e it has little intrinsic income. However, then that bitcoin is wrapped to it can be used within DeFi it becomes an asset that can have extrinsic value. When the wBTC is deposited as collateral, it can directly generate yield (currently 0.01% on AAVE or Compound) and, as collateral, it allows the holder to access additional money making opportunities. This means that the holder can decide what level of productivity (and additional risk) they want to have with their BTC.

Likewise, stable coins are intrinsically unproductive, or may even have an associated cost of ownership. However, there are many extrinsic ways for them to generate income as yUSD, aDAI, cDIA etc.

Finally, use of liquidity mining could be considered a way that a token can have extrinsic productivity (although frequently at the risk of divergence loss when it is related to providing liquidity on exchange markets).

Intrinsic productivity for index funds

As a holder of passive tokens, an index fund is inherently unproductive, it merely represents the token prices of the underlying assets. There are a number of ways that the fund can be managed to generate income for the fund managers and token holders. I’m going to concentrate on methods that can be used to make the token productive for the holder.

Issue and redemption fees can be captured to encourage long term holding — at the cost of arbitrage efficiency.

For constant weight funds (e.g. those based on balancer pools)can include trading fees with the pool to extract value from the underlying token price volatility. — With a penalty in terms of arbitrage efficiency.

Funds can be constructed using the income generating analogues of the underlying assets (e.g. replace YFI with yYFI, AAVE with aAAVE). This is an obvious way to improve the attractiveness of the fund. However, there is an associated cost in terms of additional smart contract risk and liquidity of the underlying tokens may be significantly lower. Such considerations may make the fund unattractive to some holders. (This is the approach that pieDAO have been using with the PIEvaults launched in 2021)

For market cap based funds, it is possible to remove some of the underlying tokens to take advantage of income generating opportunities while maintaining the benefits of liquidity of the native tokens. Such an approach is not possible with the balance pool type fund design as all the tokens need to be available for ongoing trading while a market cap only needs periodic rebalancing). [Note The INDEXcoop community have been discussing this approach recently and I’ll describe one possible approach in a future blog].

Note that as they don’t contain the underlying tokens, synthetic index funds can not capture any intrinsic productivity for the holders.

Extrinsic productivity opportunities for index funds

Extrinsic productivity for an index fund really relies on external mechanisms to build on top of the fund token. One common method is to use the fund as be basis for a Liquidity mining programme, although this is normally short lived as it requires an external source of value to generate the rewards.

Compared to a single token, an index fund has the inherent benefits of downside protection and reduced volatility (Table 1).

Reduced volatility combined with downside protection can make the index fund more attractive as a collateral (See figure 1 for $DPI on cream.finance). Being added as collateral means that the index token holder has the potential to put their tokens to work, even if only to borrow stable coins to capture low risk yield.

As more collateral options become available (Compound, AAVE, MakerDAO etc), and the total AUV for the fund increases, then the fund token becomes more attractive for more active yield generation such as the methodologies used by yearn to maximize yield from deposited tokens.

DeFi infrastructure that allows an index to become more productive

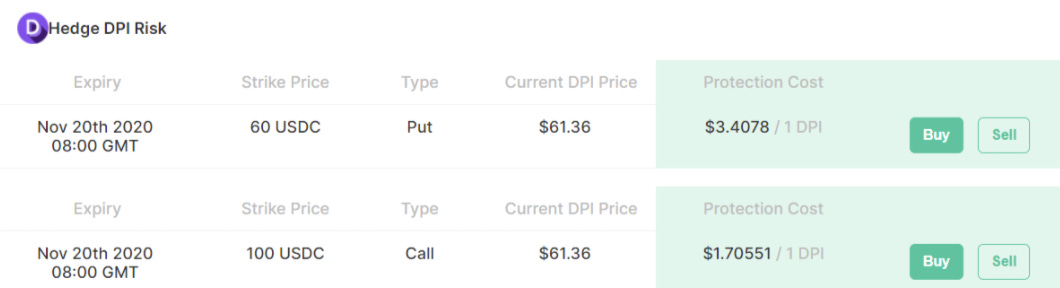

In addition to the direct income from being used by other protocols as collateral, the token and fund infrastructure can be built into other DeFi protocols. For example the availability of put and call options allows traders to access protection against more general market movements (Figure 2).

Insurance for the underlying potocols increases the attractiveness of the index for some customers and allow them to make larger trades based on the fund.

Final Thoughts

Crypto index funds have the potential to be productive. Intrinsic productivity requires careful consideration of the different approaches and their consequences. Extrinsic productivity generally requires other DeFi protocols to recognise an opportunity to benefit from the available capital and the inherent benefits of diversification and downside protection.

Disclosure and Disclaimer

I’m a long term investor in cryptocurrencies including DeFi. I am an active member of the INDEXcoop which manages the $DPI fund.

This is not financial advice, all investments are risky, crypto investments are riskier than most. Do your own research. Do not invest more than you can afford to lose.