INDEXcoop - Metamorphosis for Owls

A personal review of the coop after 2 years

TLDR

Since October 2020 INDEXcoop has been re-inventing itself as an organisation from an experiment born of two companies to a decentralised organisation dominating the decentralised structured product sector of DeFi.

This is my utterly biased stream of consciousness for the first 2 years.

An experiment in DeFi Summer

During mid-2020, DeFi Pluse Inc launched $DPI built on Set Protocol v2.0 to produce a diversified basket of DeFi governance tokens for users to issue and hold. The thesis was simple, passive baskets were a dominant asset class in traditional finance and many investors understood the benefits of holding the entire market.

Initially, TLV was slow to build as such a dull proposition did not attract the crypro degens who were enjoying the “free money” of DeFi Summer. As a result SET and DFP apparently decided to bootstrap a new DAO with its own token and a mission to drive the adoption of structured products (built on SET protocol).

It is my view that both SET and DFP considered this as an experiment which could flourish or fail, but one that was worth attempting amongst all the other DeFi launches and food farms.

Launch Tokenomics

For defi Summer, the tokenomics were pretty vanilla:

2% to Defi Plulse Inc (vested)

28% to SET Labs (vested)

1% as an Airdrop to $DPI holders.

9% as a launch liquidity mining programme on $DPI over 60 days. (#15,000 INDEX per day)

52.5% to community treasury over 3 years.

7.5% as a Methodologist programme (over months 2 to 20)

#1 and #2 gave the founders a substantial, but not controlling, stake in the coop, #3 and #4 meant that the majority of initially circulating tokens were decentralised with the community treasury #5 growing over time.

Methodologist programme

The methodologist programme #6 was intended “to attract and reward index methologists a share of emitted tokens based on the success of their indices”.

Personally, I think that this was a flawed mechanism, particularly as one of the first decisions of the DAO was to focus all efforts on growing $DPI which effectively removed all competition between methodologists to capture that 7.5% of supply. Thankfully, the programme has now expired.

Community and Structure

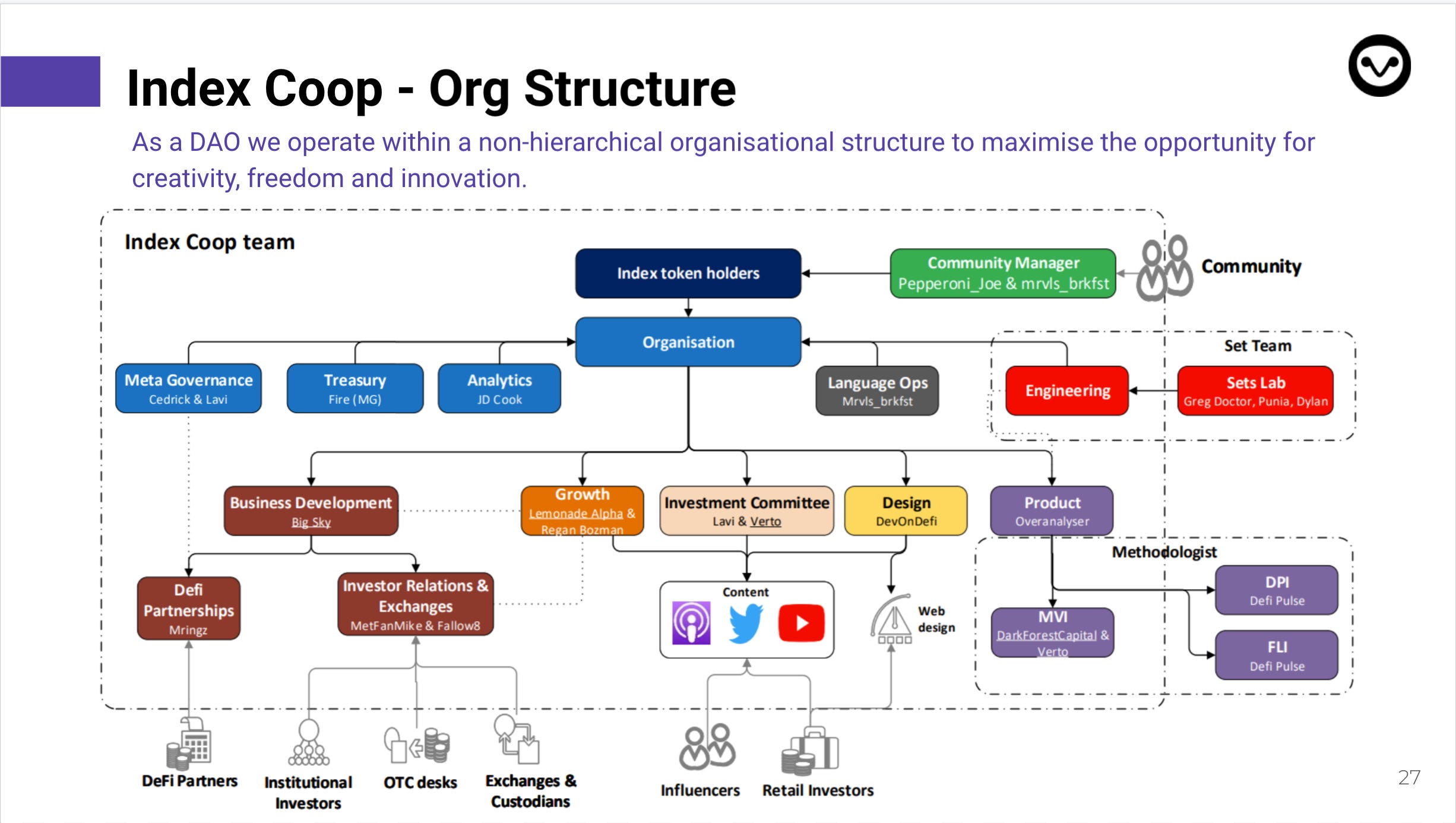

Perhaps the biggest metamorphosis for the coop has been in the structure and personnel.

In October 2020 new community members joined an entity created by Set Labs; SET owned the deployed contracts, the discord, discourse, Medium, website, twitter, snapshot etc. SET employees planned meetings, prepared the decks, held 1 to 1’s and were basically doing everything.

The October 2020 rewards distribution included 11 community contributors (and 12 others who got 30 $INDEX for attending the first governance call! ). It’s interesting to note, that none of these individuals is significant within the current coop (zero contributor rewards in September 2022).

By April 2021, 4 community members had been given “Full-time contributor” roles with 24-month agreements. There were a further 4 working group leads with stipends agreed upon in advance (with 35 other contributors and 15 other bounty recipients). Once again, it’s interesting to note that none of these core 8 people who were the backbone of the coop 18 months ago is involved in the coop’s current operations and non received any contributor rewards in September 2022.

By mid-2021, the community was expanding rapidly and with an onboarding process that set the standard for DeFi (complete with Org charts and contributor questionnaires).

Personally, I felt like the coop became bloated at some point in 2021. While we needed the community to grow, a similar growth in contributors (and costs) was not sustainable. We also attracted many, many, many product ideas. And there was an expectation that we should (and could) launch everything.

With a push from Set and 1KX in April 2022, the coop looked at restructuring and downsizing significantly. This resulted in a number of full-time contributors being let go, and a significant cut in flexible contributors.

In August 2022, the council provided an update capturing the rebirth:

40% reduction in contributor spend

With over 60% of September 2022’s budget being spent on Building (vs Growth and Service)

Note, liquidity mining and the methodologies programme had long since stopped

Risk off treasury management

Completed transfer of ownership of smart contracts, keepers and treasury assets.

Reviewing alternatives to Set protocol when it’s a better fit for the product design.

Now it feels like the coop is much better organised, and focused and is building through the bear market.

Perhaps the final hurrah of the 2021 coop community/contributor massive was Permissionless in May 2022 when owls from all over flocked to West Palm Beach to meet face to face.

How the coop differs from other DAOs

I think that one of the ways that the coop differs from many other DeFi protocols is due to how we formed. From what I have seen, most protocols are formed by an individual / small team (the majority of whom were Devs), then added individual contributors as they grew.

Conversely, the coop started with a core product and threw the doors wide open to undergo an explosion of contributor addition. Then we scaled back to the current core. I also think that, compared to other protocols, the surge in contributors was weighted towards non-Dev talent. The coop in 2021 was really focused on growth and Business Development (with Engineering still dependent on SET labs). The eventual transition to a builder focus has been interesting to watch.

Where are they now?

With the hugely effective onboarding system in 2021, modifications to the structure and the recent downsizing, it’s inevitable that many of the very talented and driven Owl alumni would be spread far and wide within the DeFi ecosystem.

At the risk of missing too many, I’m aware of owls have migrated to:

Company employees Set, DeFi Pulse, a16z, 1kx network

DeFi DAO contributors AAVE/Lens, Llama, Inverse, Synthetix, Polygon, BanklessDAO

DeFi DAO founders; Metaportal, D4

NFT projects, XONE, Buzzed Bears

And our competitors…

Financial Management

Financial reporting is one of the few things that has not changed significantly over the last 2 years. Contributors immediately took ownership of analysing the finances from the start and have done an excellent job in reporting the treasury assets:

In addition, the Treasury and Business Development groups arranged strategic sales of $INDEX to large partners (@$24.26) in early 2021 for USD to secure a strong runway of assets to see us through any potential bear markets.

Metagovernance

One of the coops core value propositions lies within the ability to participate in Metagoverance. Metagovernance allows INDEX holders to participate in the governance of other protocols using the tokens held within their products smart contracts. While not all governance structures allow the coop to participate, we are able to vote within Compound, Balancer, Barger, Yearn and Uniswap. However, perhaps the most effective application of INDEXcoops metagovernance power is within AAVE where we have been able to propose (and vote) on governance including the listing of $DPI within AAVE v2.

Personally, I think Metagovernace is extremely valuable, and it should be wielded by INDEXcoop for the benefit of INDEX holders and the users of our products.

Current status

I see the coop has gone through many different changes over the last 2 years with the overall impact of making a sustainable organisation:

A smaller, more focused contributor group.

Secured USD treasury assets to secure more than 2 years of runway.

A total stop on liquidity mining

A more secure legal structure based on a Caymen Foundation

Our future growth is no longer determined by SET labs nor DFP.

Taking full Engineering control over product and rebalancing.

A move from simple basket products, to leverage products, to the current focus on yield.

INDEX and DPI are listed on Gemini and Coinbase.

Products are available on Mainnet, Polygon, Loopring, zksync, Gnosis chain and Argent.

Combined, these can only help the coop weather the current bear market and be well positioned for growth with new products built on a foundation of income generating products:

Final Thoughts

The coop is constantly evolving as different people contribute, products are launched and the DeFi landscape evolves. The planned transition away from SET control is complete and the core community feels much more confident in its direction. I’m personally very optimistic on what Ophelia and her fellow owls can achieve.

Coop vs Co-op

Owls are frequently asked whether the organisation should be pronounced “Co-Op” as in cooperative) or “Coop” (as a building for birds). This has caused many heated arguments (and ruffled feathers) amongst the community. Personally, I’ve always called it the Coop.

P.S. I’m currently drafting part 2 of this retrospective looking at AUM, products and liquidity…

Finally, if, you want to know more about INDEXcoop, you can find more info on the website, Twitter, or sign up for the weekly newsletter and have a look at the guide to earning yield on digital assets.