Market cap vs equal weight index funds

Market cap vs equal weight index funds

Originally published in my old blog 25 October 2020

This is part of a series of posts looking at index funds, how they work in TradFi and DeFi. Future parts will be linked at the end.

TLDR: Part 1: Diversification is a good thing for most investors

TLDR: Part 2 — Market cap weighed funds are simpler to implement, but fixed weight may deliver better returns.

Index vs Fund

Most investment index funds provided by asset management companies are based on indices produced by 3rd parties. E.g. there are multiple funds available that aim to track the S&P 500. In this case S&P are the index methodologist, and the funds are created by Vanguard, Blackrock, etc. By separating the asset holding from the index construction, each company can specialise and it allows the asset management companies to compete on the execution of the passive fund, and not fund component selection (which is what active funds do).

As the financial markets move, and companies grow /fail /merge, the index methodologist (S&P, FTSE, etc) will change the composition of the index by adding and removing shares from the overall list. Then the fund management companies adjusting their fund compositions to best match the index. This typically happens every 3 months.

Market capitalisation weighing

In TradFi the most common method used to construct an index (and thus funds based on the index) is market cap weighing. This is simply allocating a proportion of the funds value to each underlying component based on their relative market caps.

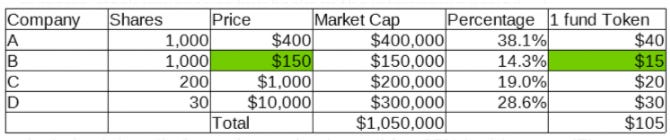

So, for a simple fund covering 4 shares, with a combined market cap of $1 M, the index would consider each as a proportion of the total market cap (40, 10, 20 and 30% respectively). Then the fund management companies will decide on a starting price for a single unit each will represent a fraction of the overall market cap. A $100 fund unit would represent ownership of $40 of share A, $10 of B, $20 of C and $30 of D.

Now suppose that share B gains 50% to give a share price of $150. The coverall market cap increases to $1.05 million, and the % of each component within the fund changes (Table 2). However, when looking at an individual components, the value of A, C and D are unchanged while the value of B within the fund unit has increased by 50% from $10 to $15.

Another way of looking at this is to think about the components that make up a single fund unit. In Table 1, one unit represents 1/10th of an A share, 1/10th of a B share, 1/50th of a C share and 1/33.333 of a D share). After the change in B share price, 1 unit of the fund contains exactly the same fractions of the underlying shares. This means that you can effectively take paper share certificates in the correct market cap ratio, lock them in a safe for 5 years and at the end you will hold a correctly balanced market cap portfolio. (Assuming of course that there have been no additions, removals, mergers, stock issuance or buy backs in the intervening period…).

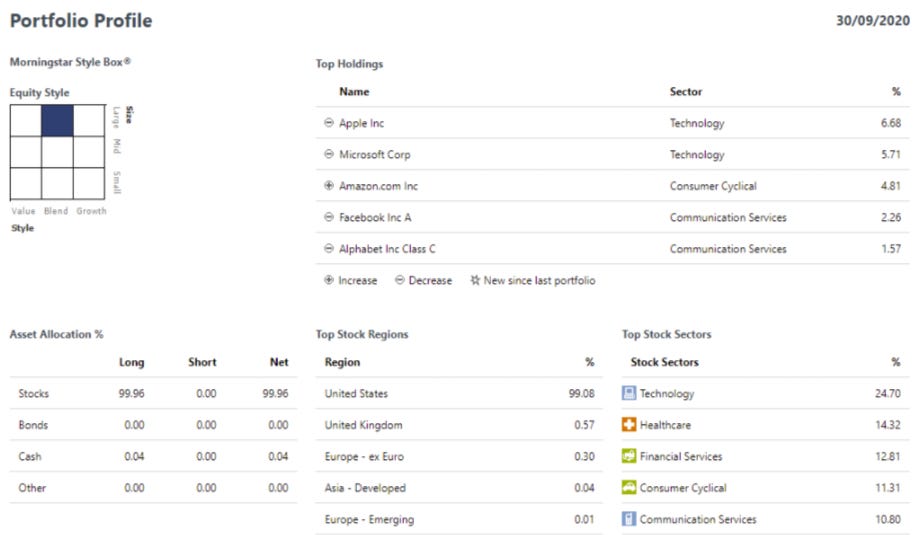

One criticism of market cap weightings is that they can become very focused on a small group of companies / sector. For example, the top 6 shares within the current S&P 500 fund make up 21% of the total fund value and the index is heavily focused on technology with ~35% in this sector (Figure 1). The FTSE 100 has a similar imbalance with 24% being held in the top 6 shares and leaning toward consumer defensive stocks.[One way of preventing this is to place a cap on the size of an individual member of the fund]. These imbalances change over time as the market moves, af ew years ago the FTSE 100 index was dominated by financial services and oil.

Equal weight index

An alternative to market cap weight is to fix the % composition of the fund at the start and then have the fund track the share prices and those compositions. Using the same starting point (table 1), and the same 50% increase in share B price, then in order to maintain the target percentages, part of B will be sold and used to buy the other shares. This results in the same increase in the unit value ($100 to $105) but differences in the holdings:

So, while the market cap fund sees a change in the % within the unit, the equal weight fund maintains a constant mix. However, the relationship between a unit and the underlying shares changes. After the increase in share B price each unit now represents 42/400 of A shares, 11/150 of B, 21/1000 C and 32/10,000 D). Basically following the increase in B, some of each of the underlying shares has been purchased, or sold, to maintain the equal weights.

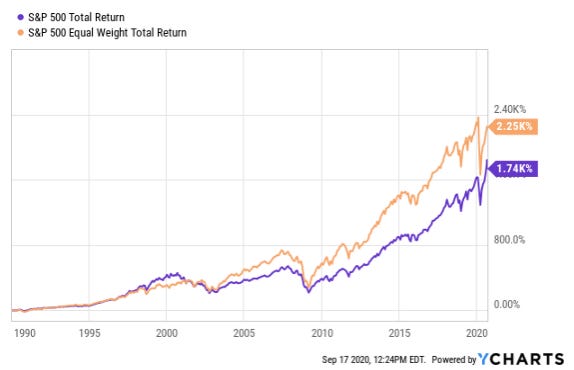

At first glance this may not make sense as you are constantly selling the best performing shares However, back testing the S&P 500 (market cap) against a equal weight fund using the same components actually shows the latter out performing over long timer periods (Figure 2 — no reference available — sorry).

Final thoughts

In TradFi, the majority of funds are market cap based. This is because the fixed weight methodology requires constant purchase and sale of shares to maintain the target weights. This adds significant complexity and cost to fund management.

This post is part of a series of posts looking at index funds, how they work in TradFi and DeFi:

Part 1: Diversification is a good thing for most investors

Disclosure and Disclaimer

I’m a long-term investor in cryptocurrencies including DeFi tokens and indices.

This is not financial advice, all investments are risky, crypto investments are riskier than most. Do your own research. Do not invest more than you can afford to lose.

Twitter: @AnalyserOver