Of whales and shrimps - A Uniswap pool

A swim in the first 136 days of the $DPI:ETH uniswap pool

I’m heavily involved in the INDEXcoop community who manage the $DPI DeFi fund token. Since joining the coop, I’ve found that I have an (unnatural ?) interest in the structures of such funds and how they work. Recently we have been discussing who uses $DPI, how they use it, and how we can cater for their desires.

JD recently did some excellent analysis of $DPI holders and retention which he captured in a recent forum post and tweetstorm [wen Blog JD?]. I’m trying to do something different and looking solely at the Uniswap pool as this is the largest liquidity pool, and the only that the coop has been liquidity mining.

Note, this data set isn’t perfect, and I can’t see all the details I would like, but the gross trends are apparent.

Trends in $DPI issuance and liquidity provision

$DPI is an index fund token, the number of tokens varies overtime as they are issued or redeemed. Issuance requires deposition of the governance tokens in the correct proportion (a multiple of the weights published by the methodologist (DeFi Pulse).

$DPI was launched in mid September with initially few tokens issued. There was a rapid expansion of the number of tokens on the 6th October, then the INDEXcoop was launched along with a liquidity mining programme on the $DPI:ETH pool using 15,000 $INDEX tokens per day. At the start of the liquidity mining programme, over 85% (154k of 180k on the 20th October) of all the $DPI was sitting in the liquidity mining and the coop was concerned that we would see cliff in $DPI circulating as we the rewards dried up. In November there was a significant rise in DPI issued (due to a spike in $INDEX price following mentions in Crypto YouTube channels).

Obviously such liquidity mining is unsustainable in the longer term, so the coop is trying to find a balance between reduced rewards while maintaining Assets under Vault (AUV). The goal will be to have a large liquidity pool to allow large trades with minimal slippage with no ongoing costs.

As expected at the end of the initial 60 day liquidity mining programme on the 6th December, there was substantial redemption of $DPI. However, this stabilised at around 200,000 %DPI tokens. This was partially maintained by a second liquidity mining campaign in December for 3,864 $INDEX per day, and a third campaign in January for 2,500 INDEX per day.

Overall, the liquidity pool value (Figure 2) shows a similar trend with a steep climb in early October, a peak in November and falling off in December. However, the increase in both $ETH and $DPI prices means that the pool actually contains fewer tokens. Currently the Liquidity pool only contains 91K $DPI, which is 35% of the $DPI in circulation.

Note that this pool is currently subject to liquidity mining by both INDEXcoop and HARVEST. In addition, a number of other farming programmes are being run by Linkswap, Sushi and a Loopring pool has just started.

Analysis of the Uniswap pool

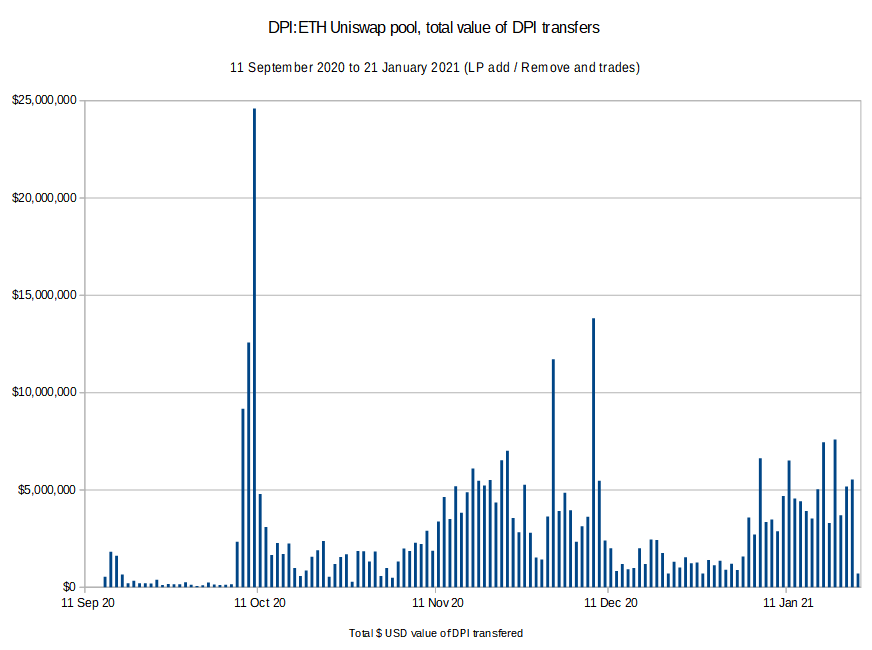

At the time of downloading, etherscan identified 41,697 on-chain actions that relate to this pool. Combination of the number of DPI transferred in each transaction, and the CoinGecko opening price for each day allows the total $DPI value to be plotted:

This shows the similar trend to the circulating $DPI, and pool AUV. With lots of action in early October, mid November and early December. As with the pool AUV, there is a growth of $DPI transfers into 2021.

Note, this analysis is based on the Etherscan interaction of $DPI with the pool. This includes $DPI purchases, sales, as well as addition and removal of $DPI:ETH liquidity. For trade volume information, it is better to look at info.uniswap.org . This shows that on the busiest day for the pool (9th October 2020), there was $17 M of trade meaning that there was ~$8 M of $DPI liquidity changes (and a further $8M of ETH changes).

Whale spotting

Sorting the data by $DPI size allows the largest trades over to be selected and (manually) queried on Etherscan. There have been 103 transfers (trades and liquidity) that contain over $250,000 of DPI, these have been categorised as:

25 x Liquidity deposits (with an equal value to ETH)

36 x Liquidity withdraws

13 x Arbitrage (DPI trade combined with issue or redemption in a single transaction)

5 x Farm Buys ($DPI purchase combined with Liquidity addition)

10 x Farm, sales (Sell and withdraw)

7 x Purchase $DPI

7 x Sell $DPI.

These, and a further 481 $DPI transfers worth between $100,000 and $250,000 are presented in Figure 6. Once again, this shows similar trends with activity in Early October, mid November and Early December. This quieten at the end of December by appear to be increasing in January.

Many of the larger purchases and sales of $DPI are linked to liquidity addition and removal by the Alpha Homora farm which was using leveraged farming for INDEX. Even so, it’s clear that there are some large purchases that are not directly liked to $DPI farming (this correlates to analysis of the 28 addresses holding $DPI, which found 14 addresses holding 6% of the total supply that had never moved the tokens after purchase).

The largest trade not related top farming was for $411,000 DPI on the 22nd January. As this was made with a pool with ~$40 m liquidity, it likely caused ~2% Slippage in the price. The largest trade associated with a farm was for $686,000 and likelty caused over 5% slippage in the $22 M pool in October.

So, is it all whales?

Not at all, while there are a significant number of large $DPI number transfers recorded on chain. There are lots of more moderate trades happening. Table 1 and Figure 7 present the value of transfer into rough groups.

Here the impact of whales looks insignificant compares to large numbers of trades, apparently focused around $1,000 to $2,500 and $100 to $250. (Note, that there may be some distortion of the trend based on the different sizes used for the groups) The latter was surprising to me as my memory of gas prices makes me feel that trades < $250 would consume way too much gas as a proportion of the trade size. However, the presence of small value transfers does tie in with the analysis by JD which found many smaller holders.

Table 2 and Figure 8 present the total value of $DPI transfers for each group (Remember this includes addition and withdraw of liquidity). These show that the majority of the transfer value is in between ~$10,000 and $100,000.

Final Thoughts

I started this work because I’ve been thinking about what is the optimum size for a liquidity pool in order to allow large trades with minimal slippage. There was a feeling that anything large than 1% slippage would be considered unacceptable to the user larger user. So a target of $30 m in the liquidity pool would allow trades of $75,000 with less than 0.5%.

What surprised me was that there are obviously many trades happening that have over 1% slippage and users seem contend to do this rather than make multiple purchases. The fact I never got as far as looking at any transfers less than $250,000 was also unexpected.

Obviously many such trades may be better done by direct issue from the underlying tokens (as the arbitrage bots do), and this is an area that the INDEXcoop need to facilitate and publicise.

The other surprise is the large number of transfers, that I would not consider to be viable due to the expected gas costs. It’s apparent that there are lots of people using DeFi for small transfers and that there is a ready market for L2 solutions that save gas. I think the challenge will be to allow easy access from Fiat to L2 to avoid L1 gas costs entirely.

Overall I see a wide range of $DPI users, and as figure 1 shows, that need is growing.

Disclosure and Disclaimer

I’m a long term investor in crypto currencies including DeFi. I am an active member of the INDEXcoop which manages the $DPI fund.

This is not financial advice, all investments are risky, crypto investments are more risky than most. Do your own research. Do not invest more than you can afford to lose.